Earnest Money and Downpayment are terms you’re going to come across once you start scouting for homes. While both are given by the buyer in the form of cash or cheque, they are two totally different concepts in the world of real estate. Here, we lay out which factors separate earnest money from downpayment and vice-versa.

Downpayment: Faster Loan Approval

For lenders, there’s nothing more attractive than borrowers who can lower the risk for them. The larger the downpayment, the lesser the borrowed amount. Thus, the lesser the risk if the borrower cannot pay on time or at all. Mortgage lenders typically require a downpayment that’s 3%-10% of the total purchase price (TPP). Your downpayment is deductible from the TPP, which means that your mortgage will only be 90%-97% of the TPP + interest. If you want lower interest rates, check out government-backed loans like the FHA, USDA, and VA. Sometimes they also offer zero downpayment loans if you qualify.

Since earnest money doesn’t go through the lender and isn’t involved in any lending process, your earnest money will not influence your chances of getting your loan approved. It will also not affect your mortgage and interest rates.

Downpayment: Lowers Interest Costs

As a rule of thumb, the higher the risk, the higher the interest. The more downpayment you deposit, the more chances of getting a lower interest rate. This is, however, not a guarantee. Lenders have different rules and offer varying mortgage plans, so it would be best to ask them about it. And don’t forget to compare lenders — Lender A might offer more reduced interest rates than Lender B.

Downpayment: Lowers Mortgage

Your mortgage depends on your remaining balance for the purchase price. If you deposit a larger downpayment, the lender will calculate your mortgage based on the amount not covered by the downpayment.

Downpayment: Lender-Regulated

Sellers aren’t the ones who decide how much your downpayment should be — it is your lender. Lenders also have a minimum downpayment that’s usually 3%. There are also a few lenders that accept a 1% downpayment. This is usually approved if filed together with a downpayment grant and another mortgage program. Know your options, and don’t hesitate to ask your lender about it!

Earnest Money: “A Token”

Earnest money, on the other hand, is like a good gesture. This lets your seller know how serious you are in buying the house. This is very common in homes that are under a bidding war. If you want your seller to consider your offer and not look for other buyers anymore, depositing earnest money may convince your seller.

Earnest Money: Refundable

Unlike downpayment, you and your seller can agree on what happens to the earnest money once Escrow is closed. You can either deduct that from the total purchase price, use it to pay for closing costs, or have it returned after a few criteria are met. The terms for your earnest money will also be set in a contract, so you can expect that there will be a negotiation for this.

Take note, though, that refund for your earnest money can be forfeited if you don’t proceed with buying the home. This is to make up for the seller’s lost time and opportunity.

Earnest Money: Not Required by Law

Earnest money is only agreed upon by you and your seller. The law does not require it, so you have the option of whether or not to provide it. However, once you’ve placed the terms and conditions in a contract, this is when the law comes into play. All parties should abide by what’s in agreement, including your money’s release time (assuming you want it refunded), or risk having it reported to the court.

Earnest Money: Flexible Value

Another great thing about earnest money is that it doesn’t have a minimum amount. The value solely depends on what you and your seller agree on. The amount can be a percentage of the total purchase price or a fixed value that depends on your available cash funds. Don’t be fooled, though, by the thought that the higher the earnest money, the easier it will be to convince your seller to transact with you. Some sellers are open to accepting lower offers, especially when your reason for buying and other factors align with the seller’s values.

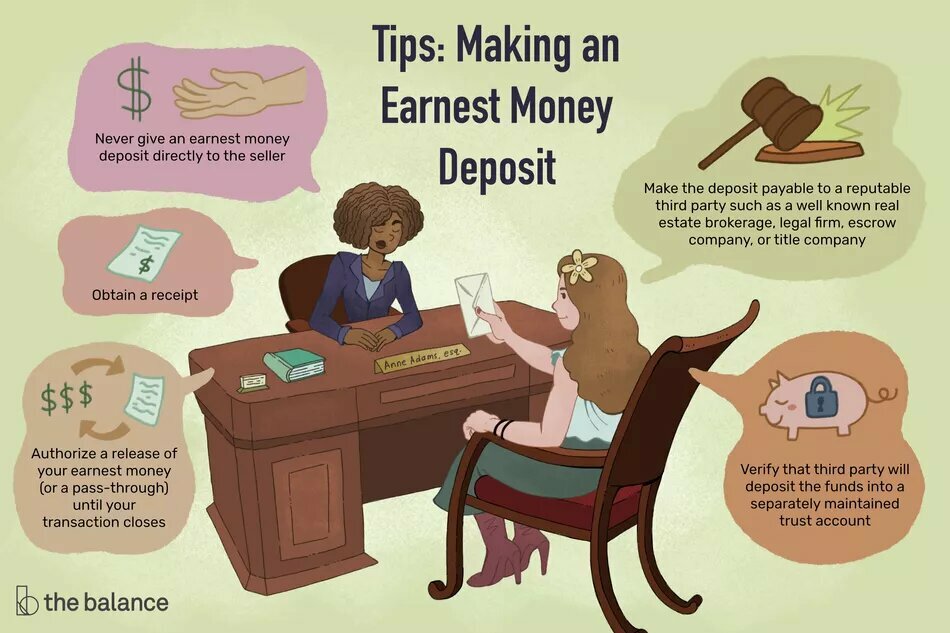

Earnest Money: Deposited in Escrow

Escrow is a third party entity legally assigned to hold large amounts of money (including earnest money) until the deal is closed. They ensure that no buyer will suddenly run off in the middle of a transaction or closing process. If any criteria or contingency surrounding the use/release of earnest money is not delivered, the Escrow has the power to hold the funds or release them to the seller, depending on the penalties stipulated in the contract.

Earnest money is also an excellent way to keep your top home options on hold when you cannot decide which one to go for yet. Likewise, there are tons of downpayment programs in the market suitable for every situation. If you want to learn more about the ins and outs of depositing earnest money and downpayment, don’t hesitate to reach out and ask us at HomeSold GA — your experienced broker in the Peach State. We can help you navigate the entire home buying process conveniently. Call us at 770-668-488 or email us through the form below!